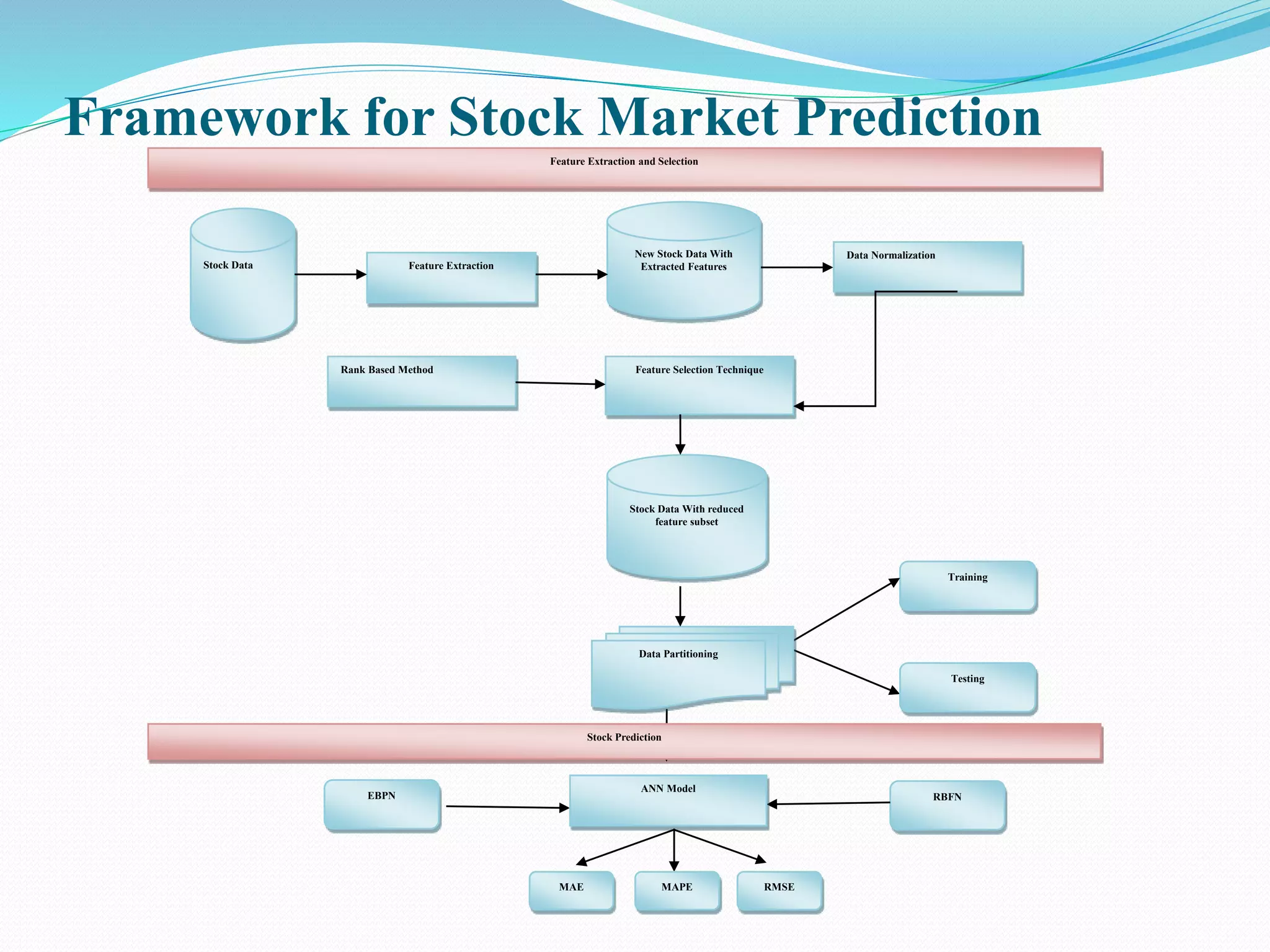

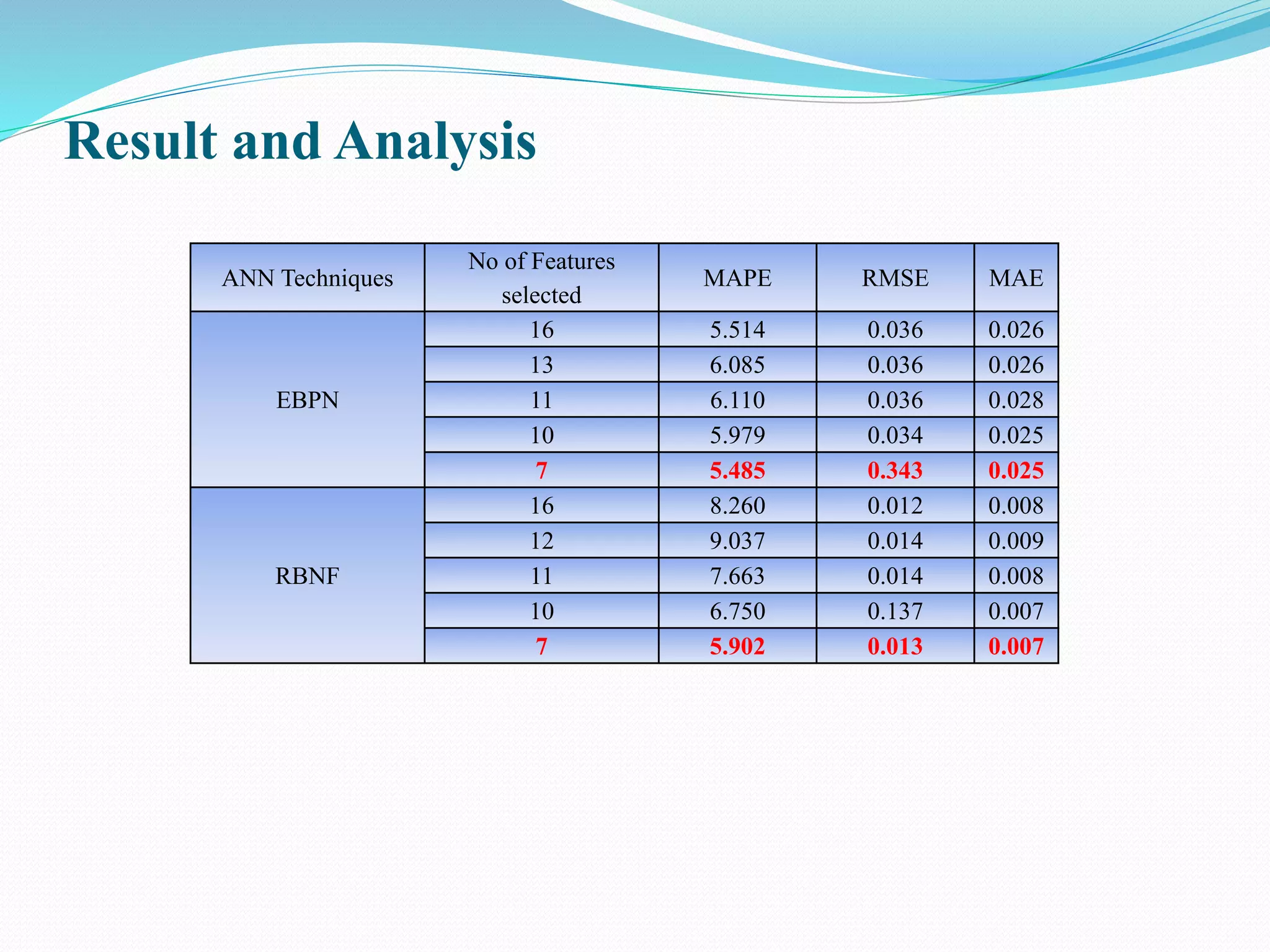

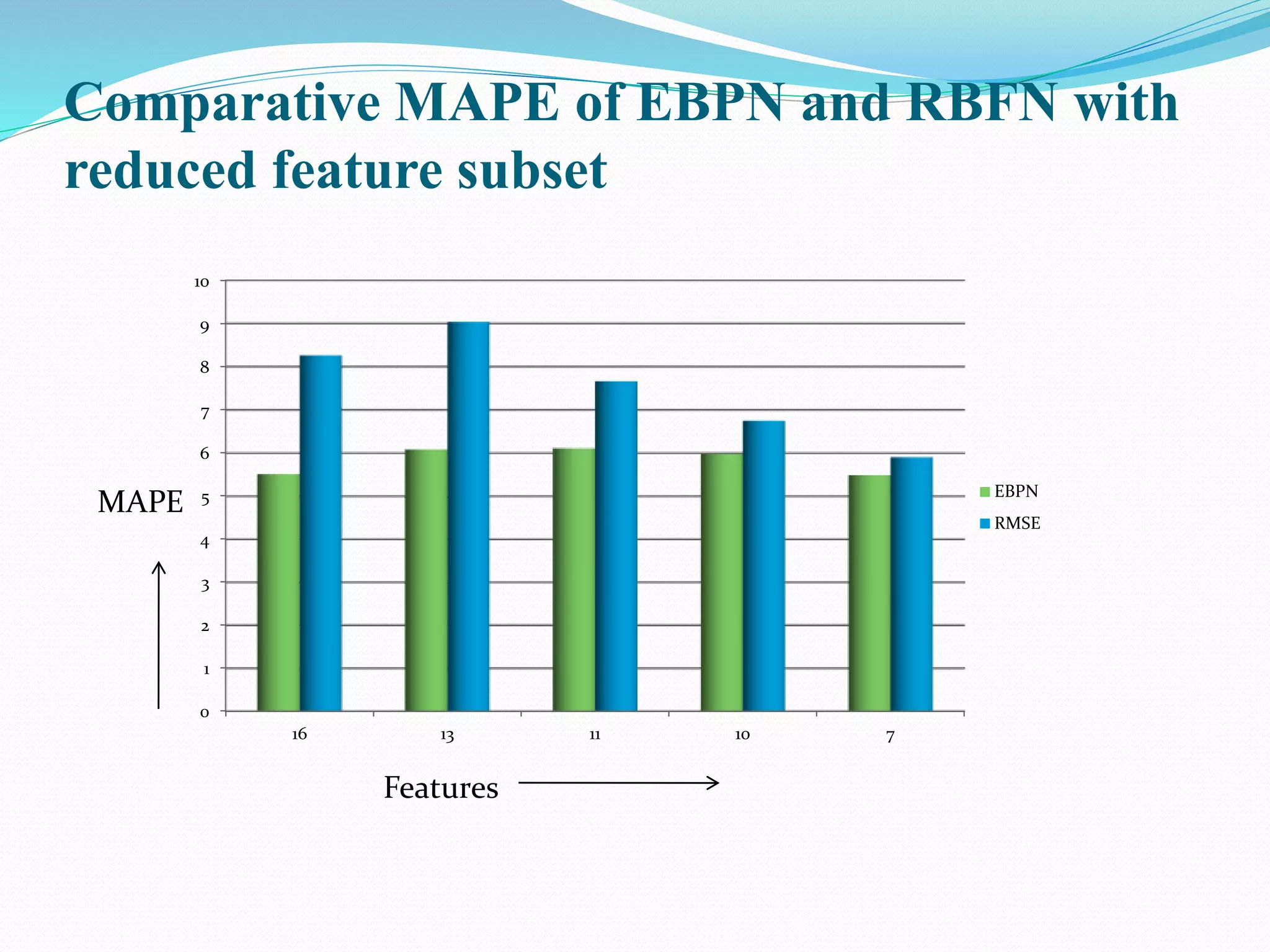

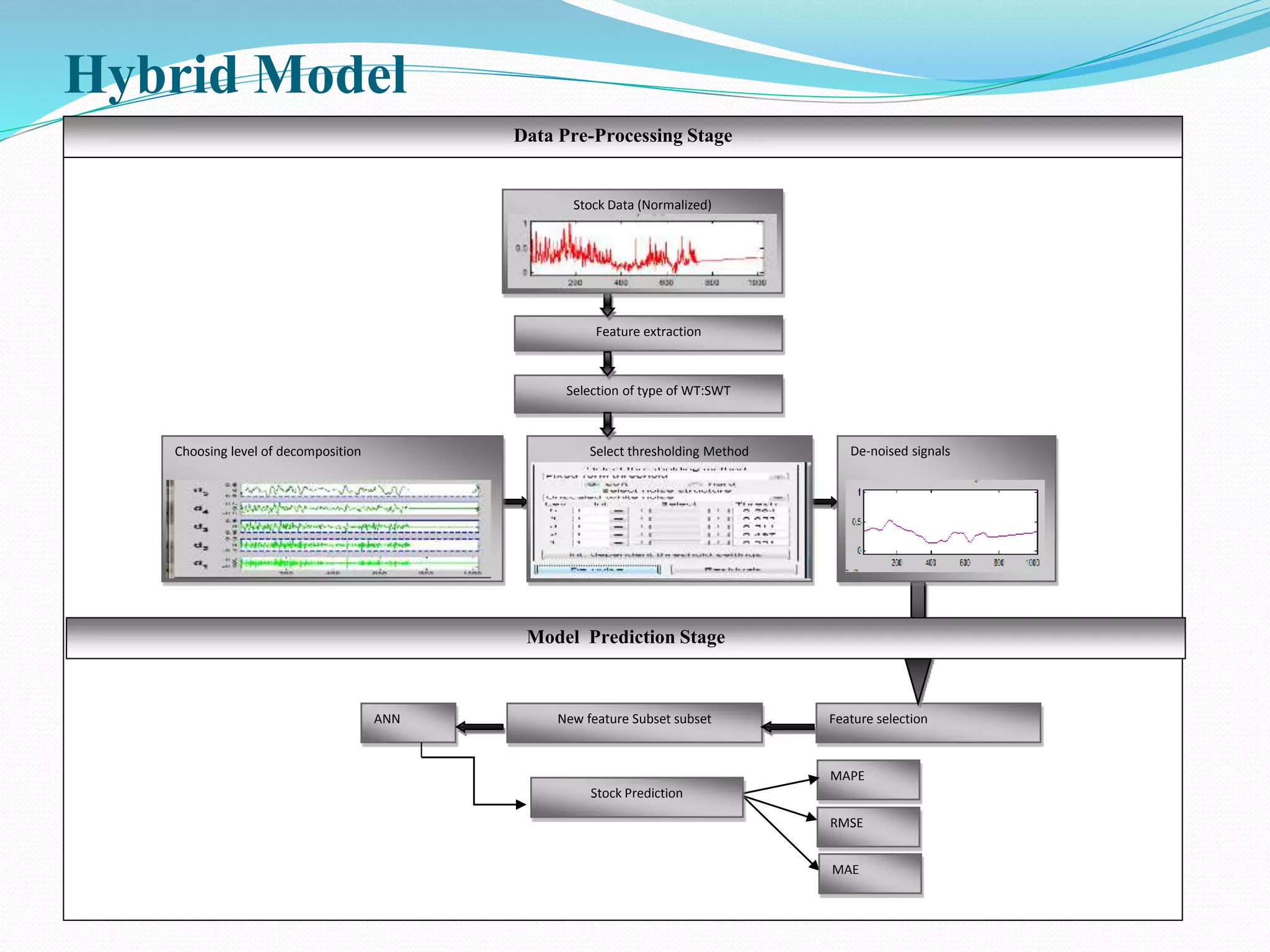

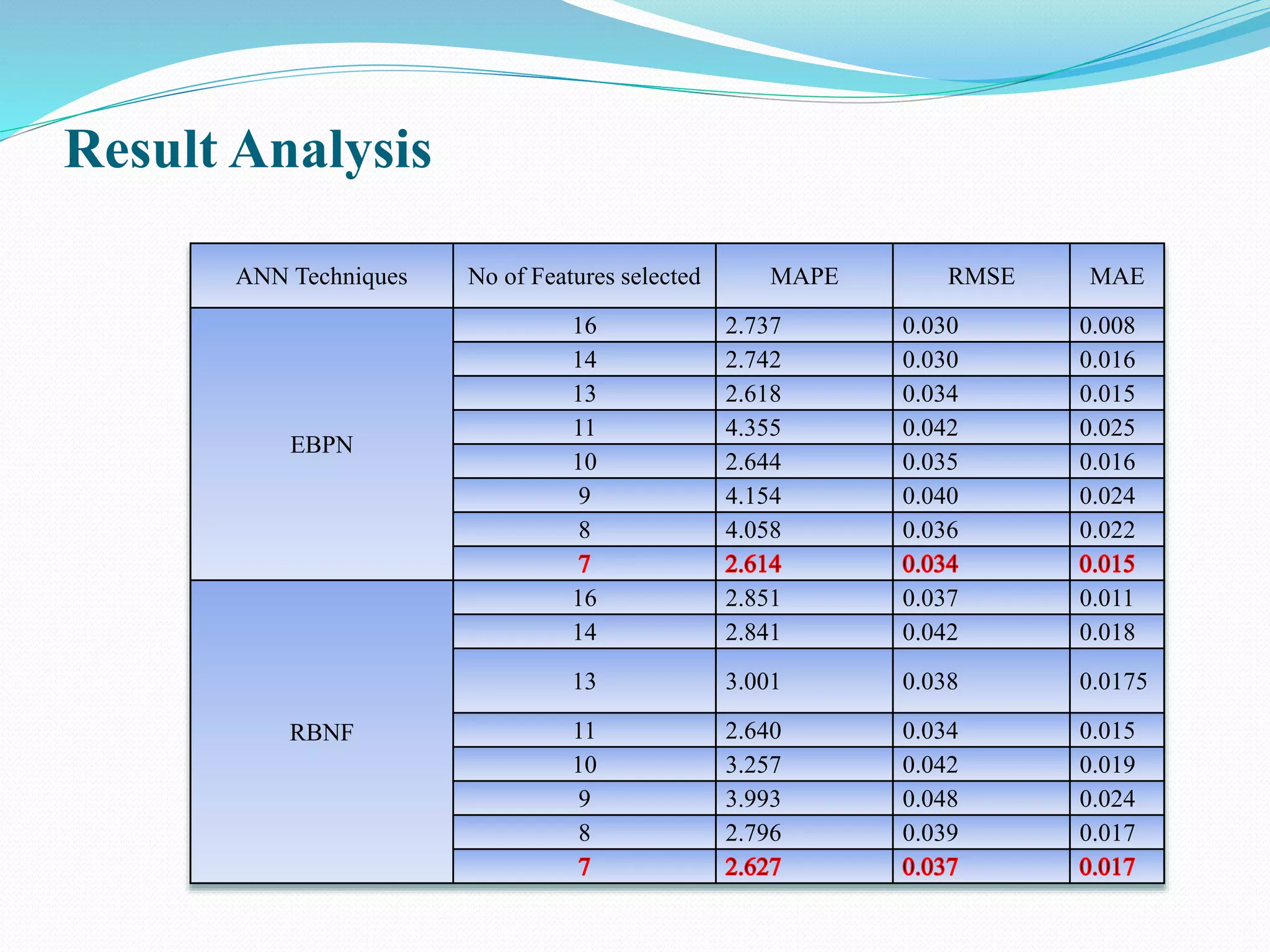

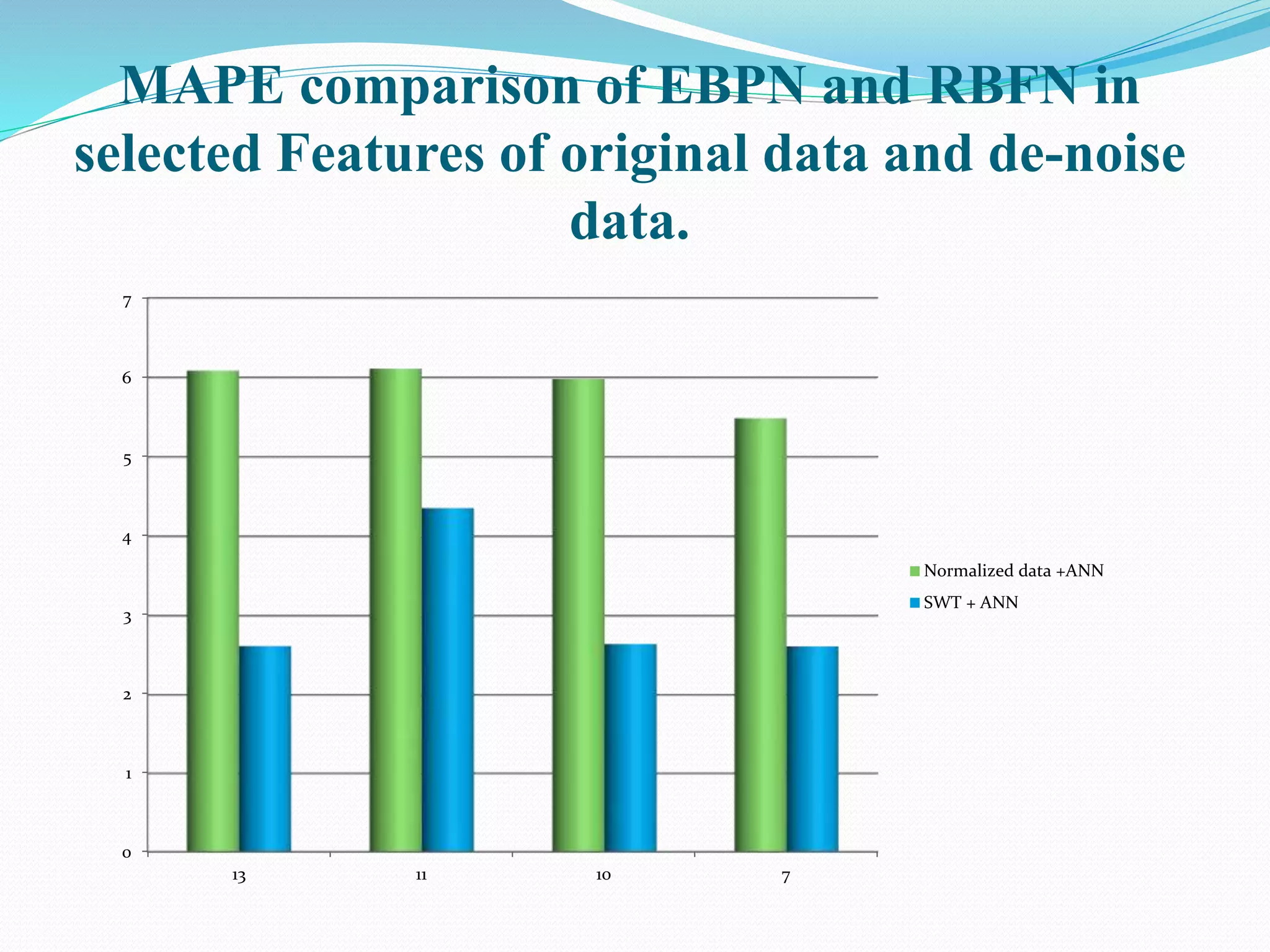

This document presents a framework for predicting stock market data using a hybrid model that combines artificial neural networks (ANN) with stationary wavelet transform (SWT) to address the non-linearity and noise in financial data. The research highlights the importance of feature extraction and selection, employing technical indicators to enhance the predictive accuracy of stock prices. Results from the study demonstrate that the proposed hybrid model outperforms traditional ANN methods, showing significant improvements in prediction metrics.